“Those who cannot remember the past are condemned to repeat it.” – George Santayana

Im agine the following game: A coin is flipped. If it comes up tails, you don’t win anything thus ending the game. If it comes up heads however, you win $1 and you get to flip again. If on this second toss it comes up heads again, you double your last payout and you are now awarded $2, and you get to flip again. If on the third toss, it comes up heads again, your payout becomes $4, and you get to flip again. The probability of each possible outcome decreases as a function of outcome size. The probability of large outcomes is very low, but not zero. The question then becomes, how much would you be willing to pay in order to participate this game?

agine the following game: A coin is flipped. If it comes up tails, you don’t win anything thus ending the game. If it comes up heads however, you win $1 and you get to flip again. If on this second toss it comes up heads again, you double your last payout and you are now awarded $2, and you get to flip again. If on the third toss, it comes up heads again, your payout becomes $4, and you get to flip again. The probability of each possible outcome decreases as a function of outcome size. The probability of large outcomes is very low, but not zero. The question then becomes, how much would you be willing to pay in order to participate this game?

This scenario known today as the St. Petersburg paradox was first introduced in September 1713 by Nicolas Bernoulli. It was then debated for close to thirty years until when his cousin, Daniel Bernoulli, presented his opinion on risk aversion, risk premium and utility in the paper “Exposition of a New Theory on the Measurement of Risk.” The following provides graphical illustrations of the outcomes as well as the probabilities of potential payouts:

The answer to this paradox gave way to the introduction of the concepts of utility function, an expected utility hypothesis, and the diminishing marginal utility of money.

In Daniel Bernoulli’s own words:

- “The determination of the value of an item must not be based on the price, but rather on the utility it yields…. There is no doubt that a gain of one thousand ducats is more significant to the pauper than to a rich man though both gain the same amount.” “The man who is emotionally less affected by a gain will support a loss with greater patience. “

Despite this dissonance, the expected utility theory remained our best understanding of how to choose rationally when we are unsure which outcome will result from our actions. However, in 1979, Daniel Kahneman and Amos Tversky published “Prospect Theory: An Analysis of Decision under Risk”; an important paper that used cognitive psychology to explain various divergences of economic decision-making from expected utility theory.

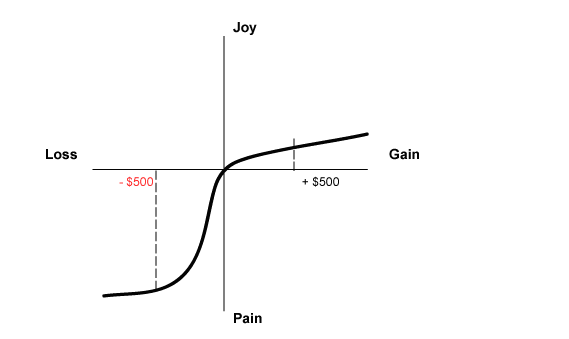

In it, they offer this theory: people don’t always maximize utility, rather people value gains and losses differently, and, as such, will base decisions on perceived gains rather than perceived losses. Thus, if a person were given two equal choices, one expressed in terms of possible gains and the other in possible losses, people would choose the former – even when they achieve the same economic end result.

For example, in a traditional way of thinking, the amount of utility gained from making a trade with a profit of $500 should be equal to a situation in which you make two trades; one with a profit $1000 and then another one with a loss of $500. In both situations, the end result is a net gain of $500.

However, despite the fact that you still end up with a $500 gain in either case, most people view a single gain of $500 more favorably than gaining $1000 and then losing $500. Further, most loss aversion studies suggest that losses are twice as powerful, psychologically, as gains.

“We have an irrational tendency to be less willing to gamble with profits than with losses.” – Kahneman & Tversky (1981)