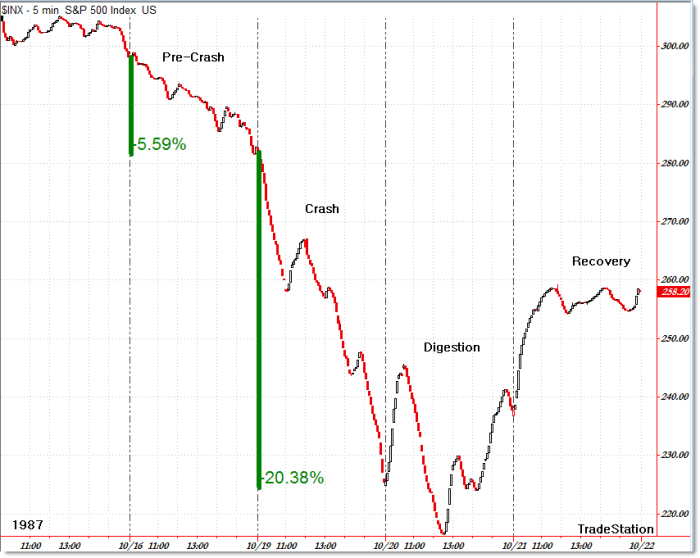

Approved in 1987, in response to Black Monday, regulators first introduced circuit breakers into U.S markets to curb significant volatility. They developed these rules to allow exchanges to halt trading temporarily in instances of exceptionally large price declines. On October 19, 1987, the S&P 500 dropped more than 20% in a single day. Let’s look at the days preceding and following this event.

Notice how the Friday proceeding Black Monday recorded a 5.6% decline, followed by the crash, digestion and recovery. That is the last time we will ever see daily volatility of that magnitude in the U.S markets. For example, under current rules, the New York Stock Exchange will temporarily halt trading when the S&P 500 stock index declines 7 percent, 13 percent, and 20 percent in order to provide investors “the ability to make informed choices during periods of high market volatility.”

I can understand how these rules are intended to restore investor confidence during a period of erratic volatility, but let’s remember the context of this mechanism. Is it supposed to invoke a feeling of re-assurance or panic?

On January 4, 2016, China implemented their own circuit breakers into their financial markets, which halt exchanges for 15 minutes after a 5 percent drop in the Shanghai Shenzhen CSI 300 Index and for the rest of the day after a 7 percent decline.

In the first week of trading in 2016, these circuit breakers halted trading twice for each respective day.

We don’t know why Chinese regulators felt that a 7% swing would be a manageable as an upper limit, but we do know that they have since decided to abolish these circuit breakers as an effective tool to curb volatility, at least for the time being.

The brief presence of these circuit breakers exacerbated losses as Chinese investors scrambled to exit positions before getting locked in. Despite the removal of these breakers from the markets, we must wonder how this impacts the rationale of the average investor to equity markets in China.

Growth in the industrial economy in the world’s second largest economy slowed drastically in 2015, and the Peoples Bank of China (PBOC) has resorted to its usual response of enhanced government spending in an effort to offset this slump.

We have to imagine what internal thresholds of pain as they relate to financial reserves need to be breached before market forces are truly allowed to prevail.