Disruptive companies aren’t new. These commercial entities tend to innovate and cater to customer needs in anticipation of their needs. Who would have thought online dating could evolve to what it has now. Who would have thought that mobile advertising could legitimately provide an alternate platform versus traditional t.v. What would the world look like if there was a majority of driver-less cars on the roads? What if drones could deliver our groceries and amazon purchases and perhaps even registered mail? “A disruptive innovation is an innovation that helps create a new market and value network, and eventually disrupts an existing market and value network (over a few years or decades), displacing an earlier technology.”

When we try and assess what value a potential disruptive company could be, we inherently have to start and assess where the business is in its life cycle and analyze the information available to us. The potential impact of the probability of this company displacing earlier industry models is what we are essentially trying to figure out.

The Uber Example

Uber is a venture-funded startup and transportation network company based in San Francisco, California, that makes mobile apps that connect passengers with drivers of vehicles for hire and ridesharing services.[1] The company arranges pickups in dozens of cities around the world.[2] Cars are reserved by sending a text message or by using a mobile app—the latter can also be used by customers to track their reserved car’s location.[3]

Aswath Damadoran – a finance professor at NYU’s Stern School of Business, published an article for his own blog titled “A Disruptive Cab Ride to Riches: The Uber Payoff.” Let’s start with the largest assumptions of his analysis and contrast that with another individual; Bill Gurley, a General Partner at Benchmark Capital and an actual investor in Uber. Mr. Gurley responded to Mr. Damodoran’s analysis, in a blog titled “How to Miss By a Mile: An Alternative Look at Uber’s Potential Market Size”

The largest point of contention is each individual’s take on (1) the size of the total available market (TAM) and (2) Uber’s likely market share.

Damodaran estimates that the global taxi and limo market is worth about $100 billion per year, but according to Gurley Uber isn’t just trying to displace the existing industry – he aims to illustrate a structured look at how traditional human car transportation can change as a result of today’s technology..

Here is Damodoran’s view on TAM and probable market capitalization.

My. Gurley offer’s his own detailed response and provides a reasonable and plausible argument that Uber’s market opportunity might be 25X higher than Professor Damodaran’s take. Let’s keep in mind that Mr. Gurley is an early-stage investor has much more access to actual data than Professor Damodaran.

I highly recommend reading both blogs to try and figure out where each person is coming from, and what you think is actually probable.

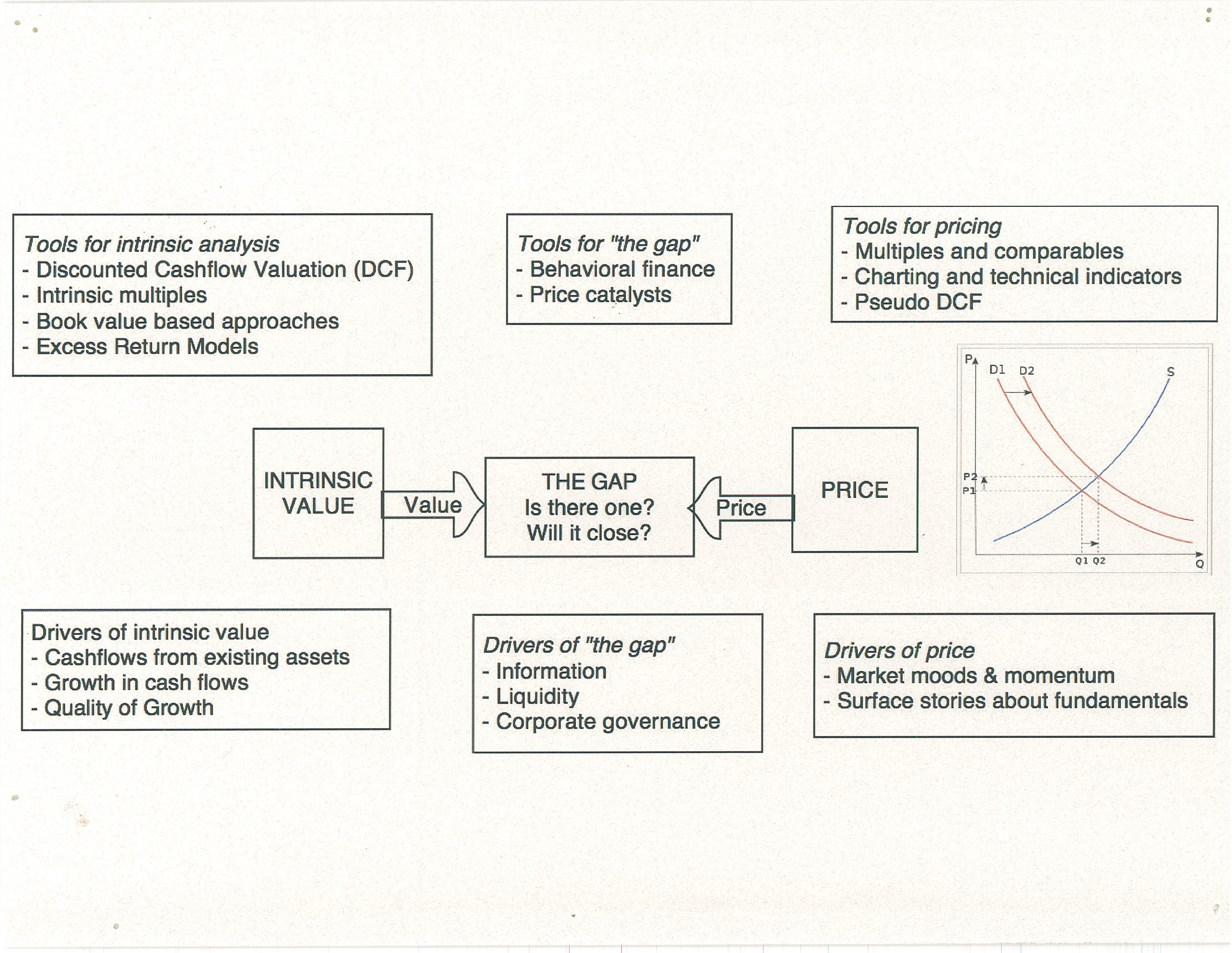

The reason I want you to think about these views are because that’s what the markets are like. A confluence of diverging views with actual positions based on their respective forecast. These views coupled with the forces of bid and ask size, determines price at any given point in time.